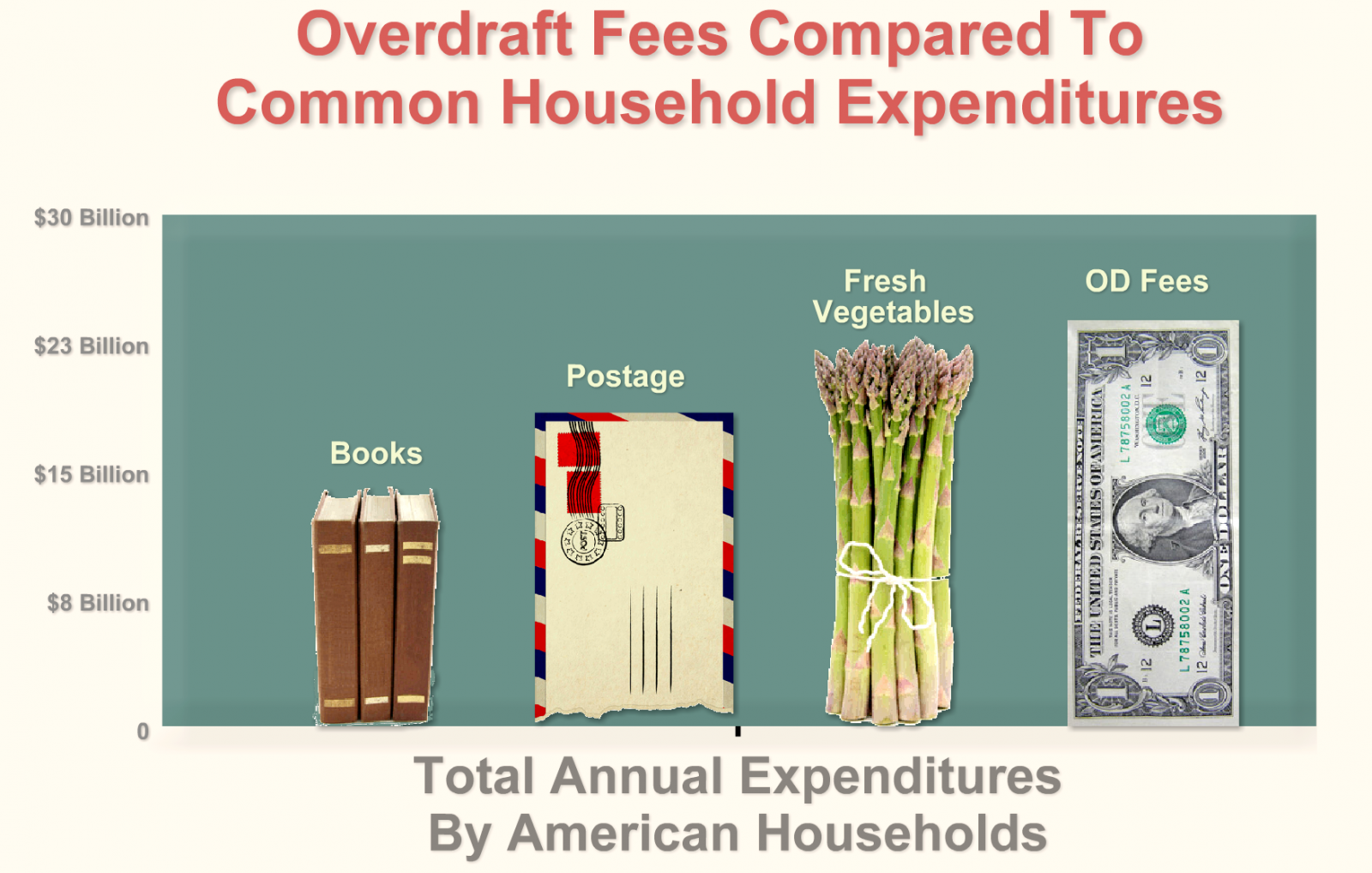

A new report from Moebs Services, a respected economic research firm, shows overdraft revenue at banks, credit unions and thrift institutions totaled $32 billion last year. That’s an increase of $400 million or 1.3 percent from 2011.

“Consumers use of overdrafts shows no indication of going away, and is actually increasing,” said Michael Moebs, who wrote the study.

At the current rate of growth, Moebs predicts revenue from overdraft fees will hit a new record by the end of 2016, topping the old record of $37 billion set in 2009.

The Moebs study found that about a quarter of the people with a consumer checking account – that’s 38 million people – frequently overdraft. The median overdraft is about $40.

More than half of the customers who frequently overdraft – 57 percent or 20 million people – go to payday lenders when they are short on funds.

Why? Because a payday loan is significantly cheaper.

“Payday lenders are the low-price source for short-term cash needs,” Moebs said. “You can get a cash advance for $16 as opposed to $25 at a community bank, $27 a credit union and $30 at bank or thrift. Those are median prices.”

While the cost of an overdrawn account has been going up at many financial institutions, the price of borrowing from a payday lender has dropped. The median charge for a $100 cash advance dropped $1.50 from 2011 to 2012, from $17.50 to $16.

Moebs firmly believes many of the people who use a payday lender would rather not, if the cost of the overdraft penalty was more in line with what the payday stores charge. He puts that price point at $20.

What it really costs to cover an overdraft

Consumer groups have long asserted that overdraft fees are revenue generators, deliberately higher than the banks' cost of providing the service.

“It’s very clear that banks are gouging customers with incredibly high and outrageous overdraft fees that are not related to their cost,” said Ed Mierzwinski, consumer program director at U.S. PIRG.

A bill introduced in Congress last week, The Overdraft Protection Act of 2013, would require these fees to be “reasonable and proportional.”

Moebs told me his costs studies, some of which were done for the Federal Reserve Bank, show the prices charged by the big financial institutions “are legitimate” because their cost structures are so high.

He estimates that a megabank makes about $3 on each overdraft charge, the same profit the payday lender earns with a $100 loan. But because the overhead at the bank is so much higher, it has to charge $30 or $35 to make the same amount.

Smaller banks and credit unions have a smaller nut to crack, so they might be able to reduce the price on an overdraft. Moeb’s advice to these institutions: lower that price and you’ll get more customers.

Cheaper alternatives

Of course, the goal is to avoid overdraft charges. Check your account statement – online, by phone or at an ATM – to make sure you don’t try to spend money that’s not in your checking account.

“If you are likely to overdraft, the main street institutions are your best choice – most credit unions and community banks and some of the thrifts – because they have a lower overdraft fee,” Moebs said.

Debit-card transactions often cause an account to be overdrawn. Remember: Your bank or credit union will deny a point-of-purchase debit-card payment or cash withdrawal from an ATM if there is not enough money in the account to cover it, unless you “opt in” to their overdraft protection plan. In that case, the transaction will go through and you’ll get hit with a fee.

A recent study by the Pew Charitable Trusts found that 54 percent of the customers who had overdrawn their accounts said they did not realize they had signed up for an overdraft service that cost money. Susan Weinstock, director of Pew’s Safe Checking in the Electronic Age Project, said this shows there is “a very high level of confusion” about how this overdraft protection works.

Herb Weisbaum is The ConsumerMan.

3 WAYS TO SHOW YOUR SUPPORT

- Log in to post comments